Mitigating Sequence of Returns Risk in Your Retirement Plan

- Feb 11

- 3 min read

Understanding Sequence of Returns Risk

Sequence of returns risk refers to the impact that the order of investment returns can have on a retirement portfolio, particularly during the withdrawal phase. Even when long-term average returns are similar, the timing of gains and losses may significantly affect portfolio sustainability when distributions are occurring.

This concept is especially relevant in the years immediately before and after retirement, when withdrawals coincide with market fluctuations.

Why the Order of Returns Matters

During accumulation years, market declines may be offset by continued contributions and time. In retirement, however, withdrawals reduce the portfolio’s ability to recover from early losses.

If negative returns occur early in retirement while withdrawals are ongoing, a portfolio may experience accelerated depletion—even if markets recover later. This risk highlights the importance of managing not just average returns, but return timing.

Sequence Risk vs. Market Risk

While market risk refers to the possibility of investment losses due to market volatility, sequence of returns risk focuses on when those losses occur.

Two portfolios with identical long-term returns can produce different retirement outcomes depending on the sequence of gains and losses experienced during the distribution period.

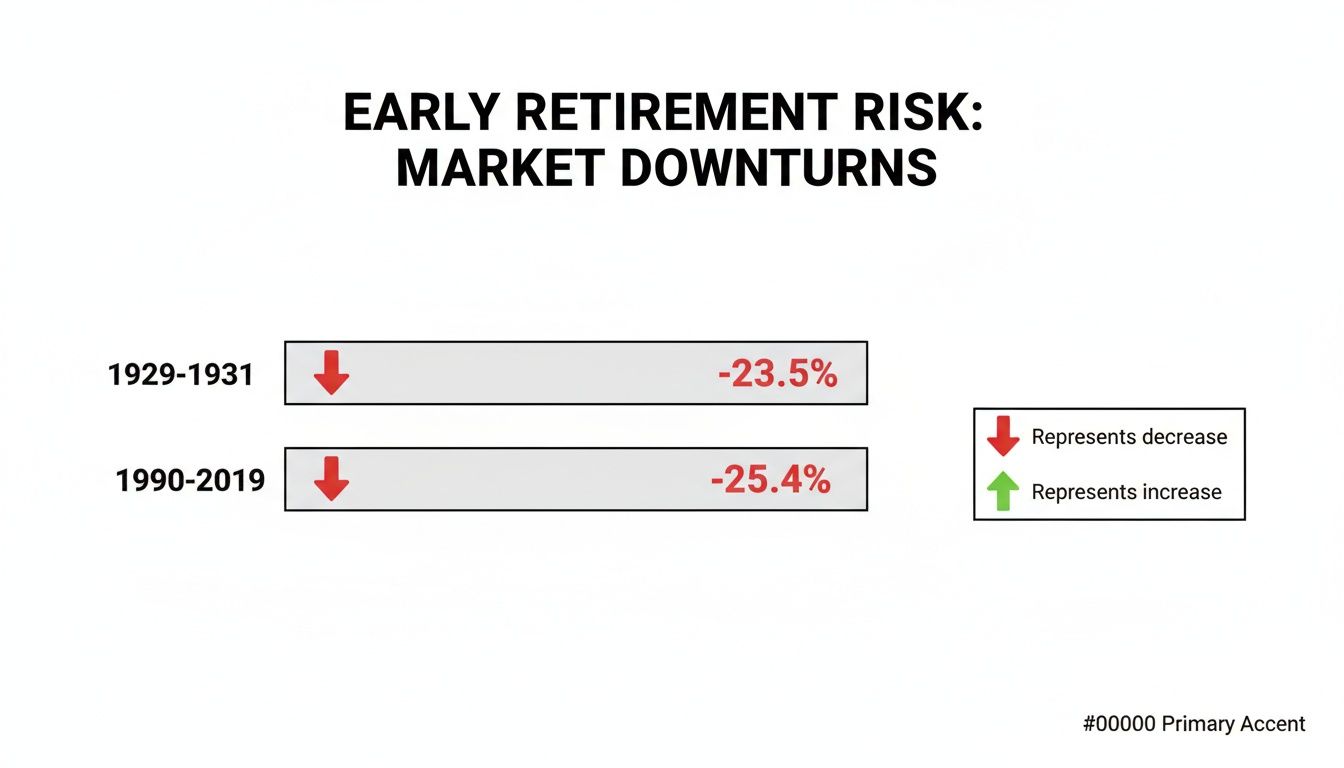

Time Periods Most Affected by Sequence Risk

Sequence risk is typically most pronounced:

In the five to ten years leading up to retirement

During the early years of retirement when withdrawals begin

Planning during these periods often emphasizes resilience and flexibility rather than growth potential.

Common Approaches to Managing Sequence Risk

Adjusting Asset Allocation

Some retirement strategies involve gradually reducing exposure to more volatile assets as retirement approaches. This adjustment may help moderate portfolio volatility during early withdrawal years.

Asset allocation decisions should balance growth needs with risk management objectives.

Establishing a Withdrawal Strategy

Thoughtful withdrawal planning may help reduce sequence risk.

Common considerations include:

Adjusting withdrawal rates during market downturns

Using flexible withdrawal strategies rather than fixed amounts

Coordinating withdrawals across taxable, tax-deferred, and tax-free accounts

Flexibility may help preserve portfolio longevity.

Maintaining a Cash or Short-Term Reserve

Holding a reserve of cash or short-term investments may allow retirees to meet near-term spending needs without selling long-term investments during market downturns.

This approach may help reduce the need to liquidate assets at unfavorable times.

Diversifying Income Sources

Relying on multiple income sources—such as Social Security, pensions, or other predictable income streams—may reduce pressure on investment portfolios during volatile periods.

Diversified income may provide stability during market fluctuations.

The Role of Guaranteed Income Sources

Some retirement plans incorporate guaranteed income sources to help manage sequence risk.

While not appropriate for every situation, predictable income streams may help offset market-driven variability in portfolio withdrawals.

Behavioral Considerations

Market volatility during retirement can increase emotional stress and lead to reactive decisions. Emotional responses, such as selling assets during downturns, may amplify sequence risk.

A clearly defined retirement income plan may help support disciplined decision-making during volatile periods.

Integrating Sequence Risk Management Into a Broader Plan

Sequence of returns risk is one component of retirement planning. Effective management often involves coordination with:

Asset allocation strategy

Tax planning

Longevity planning

Estate considerations

Regular review helps ensure strategies remain aligned with evolving circumstances.

Conclusion

Sequence of returns risk highlights the importance of timing in retirement outcomes. By understanding how early losses and withdrawals interact, individuals can better evaluate strategies designed to support portfolio sustainability.

Managing sequence risk involves thoughtful planning, flexibility, and coordination within a comprehensive retirement strategy.

Investment advice offered through Stratos Wealth Partners, Ltd., a registered investment advisor. Stratos Wealth Partners, Ltd and Parkview Partners Capital Management are separate entities. Neither Stratos nor Parkview Partners Capital Management provides legal or tax advice. Please consult legal or tax professionals for specific information regarding your individual situation. Investing involves risk, including possible loss of principal. The information presented is for educational purposes only and should not be interpreted as individualized investment, tax, or legal advice. Past performance is not indicative of future results. For more information, please review our Form ADV, available upon request.

Comments