Understanding Compound Interest as a Wealth Management Strategy

- Feb 10

- 3 min read

What Is Compound Interest?

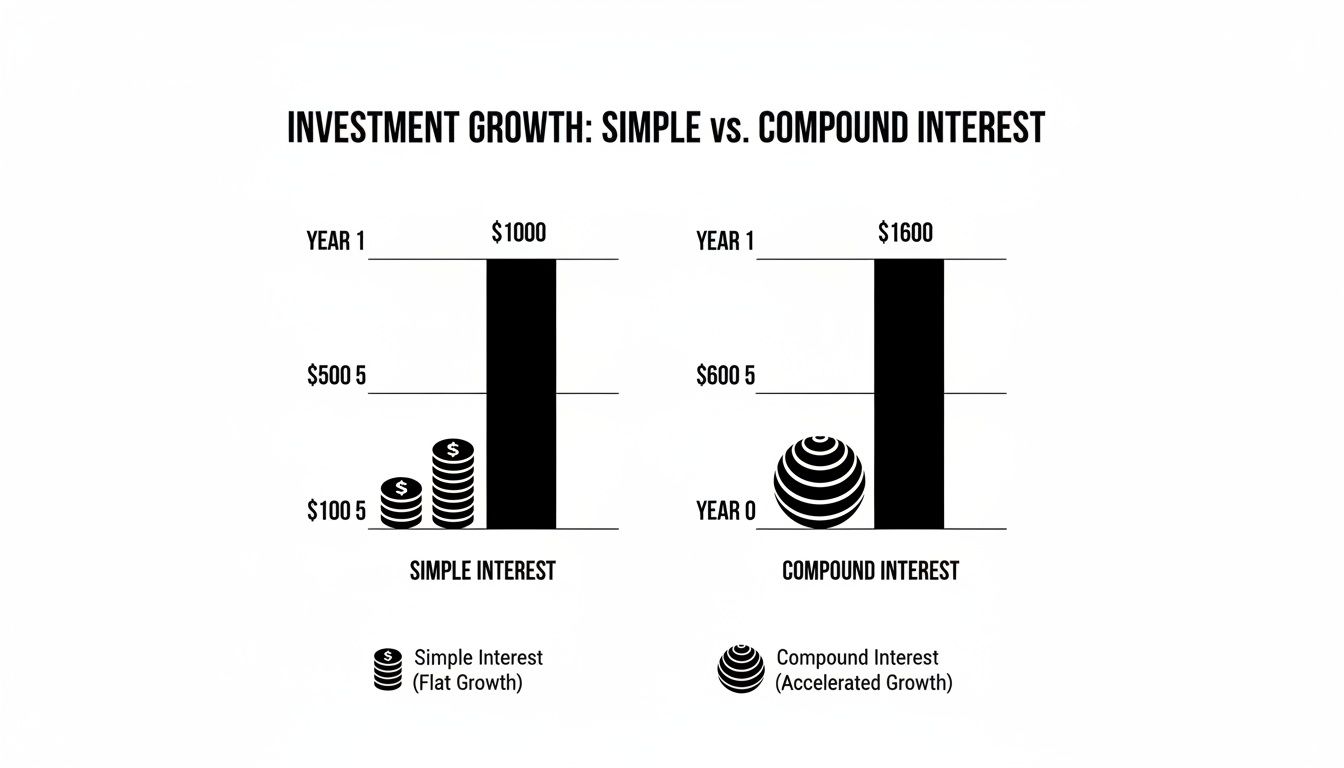

Compound interest refers to the process by which earnings are generated not only on an original investment but also on accumulated interest over time. As interest is reinvested, future earnings are calculated on a growing base, which can lead to exponential growth over longer periods.

In wealth management, compound interest is often discussed as a foundational concept rather than a tactical strategy. Its effectiveness depends on time horizon, consistency, and the rate of return after expenses and taxes.

How Compounding Works Over Time

Compounding occurs when investment earnings remain invested rather than being withdrawn. Each period’s gains increase the base upon which future returns are calculated.

Two key variables influence compounding outcomes:

Time: Longer time horizons generally allow compounding effects to become more pronounced

Rate of return: Higher net returns can accelerate wealth accumulation, while lower returns reduce compounding impact

Because compounding builds gradually, its effects may appear modest in early years and more significant later.

The Role of Consistency

Consistency in investing can support the compounding process. Regular contributions, even during periods of market volatility, may help increase the capital base that compounds over time.

This approach emphasizes discipline and long-term perspective rather than attempting to time market movements.

Compounding and Investment Costs

Investment expenses and taxes reduce the rate at which assets compound. Since compounding works on net returns, costs such as expense ratios, advisory fees, and transaction expenses can influence long-term outcomes.

Evaluating investment costs in context helps ensure that compounding is not unnecessarily constrained by avoidable expenses.

The Impact of Time Horizon

Time is often considered one of the most important components of compounding. Starting earlier may allow smaller contributions to accumulate meaningfully over decades, while shorter time horizons may limit the effect.

Delaying investment decisions may reduce the opportunity for compounding to work over longer periods.

Compounding Across Different Account Types

The structure of an investment account can influence how compounding occurs.

Tax-deferred accounts: Earnings compound without immediate taxation, allowing reinvestment of gains

Tax-free accounts: Qualified withdrawals may allow earnings to compound without future tax liability

Taxable accounts: Taxes on income or gains may reduce net compounding

Understanding account types helps frame compounding expectations.

Behavioral Considerations

Market volatility can challenge the compounding process if it leads to frequent trading or withdrawal of assets during downturns. Emotional decision-making may interrupt long-term compounding by removing assets from the market.

A structured investment plan may help support consistency through market cycles.

Compounding and Real Returns

Inflation affects purchasing power over time. While nominal returns may compound, real returns—returns adjusted for inflation—provide a more meaningful measure of long-term wealth accumulation.

Evaluating real returns helps ensure that compounding contributes to maintaining or increasing purchasing power.

Integrating Compounding Into a Broader Plan

Compound interest works most effectively when integrated into a broader financial strategy that includes goal setting, risk management, tax planning, and ongoing review.

It is not a standalone solution but rather a long-term mathematical effect supported by disciplined planning.

Conclusion

Compound interest is a foundational concept in wealth management that highlights the value of time, consistency, and net returns. While it does not eliminate risk or guarantee outcomes, understanding how compounding works can help individuals make more informed, long-term financial decisions.

Investment advice offered through Stratos Wealth Partners, Ltd., a registered investment advisor. Stratos Wealth Partners, Ltd and Parkview Partners Capital Management are separate entities. Neither Stratos nor Parkview Partners Capital Management provides legal or tax advice. Please consult legal or tax professionals for specific information regarding your individual situation. Investing involves risk, including possible loss of principal. The information presented is for educational purposes only and should not be interpreted as individualized investment, tax, or legal advice. Past performance is not indicative of future results. For more information, please review our Form ADV, available upon request.

Comments